The Trillion Dollar Equation

Based on Veritasium's video on YouTube. If you like this content, support the original creators by watching, liking and subscribing to their content.

Bachelier’s random-walk model turned option pricing into a probability problem by linking future stock distributions to expected payoffs relative to the strike price.

Briefing

A single pricing framework for options—built from physics-style randomness and later refined with real-world “drift”—helped spawn entire derivatives markets worth hundreds of trillions of dollars, reshaping how modern finance measures and manages risk. The core insight traces back to Louis Bachelier’s attempt to put mathematics around stock-option pricing when traders were still essentially bargaining over prices. By treating stock movements as a random walk, Bachelier connected finance to the same probability machinery used in heat diffusion, then used that probability distribution to compute an option’s fair value.

That probabilistic approach mattered because options are payoff machines with asymmetric outcomes: a call option can cap losses to the premium while offering leverage if the underlying rises, and a put option does the same for downside protection. Bachelier’s method aimed to make the expected return for buyers and sellers match—if an option is priced too high, fewer buyers show up; if it’s too low, everyone wants in. In other words, “fair price” becomes the price that equalizes expected gains under the model’s assumptions.

The story then shifts from pricing to hedging—how to neutralize risk using trading itself. Ed Thorpe (known for blackjack card counting) applied mathematical thinking to finance by developing dynamic hedging: adjust a stock position as the option’s sensitivity to the underlying (its “delta”) changes. This idea of continuously rebalancing a hedge portfolio becomes the bridge to the breakthrough formula that made options pricing operational.

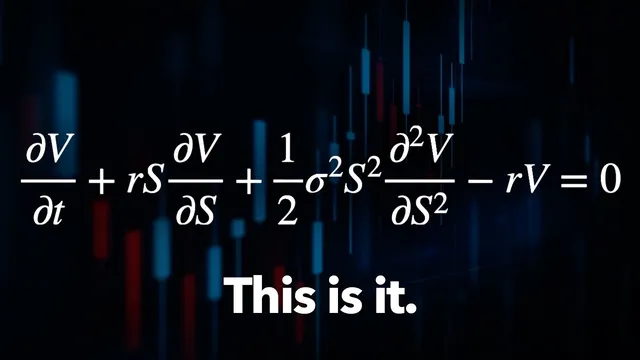

In 1973, Fischer Black and Myron Scholes published an option-pricing equation, with Robert Merton independently credited for related work. Their model improved on Bachelier by adding drift—an expected trend in stock prices rather than pure randomness—and used stochastic calculus to derive a partial differential equation. Solving it yields an explicit formula that turns inputs like volatility and time to expiry into a concrete option price. That explicitness is what accelerated adoption: within a couple of years, the Black-Scholes benchmark became standard on Wall Street, and exchange-traded options volume surged. The Chicago Board Options Exchange was founded the same year, and derivatives markets expanded rapidly, including credit default swaps, over-the-counter derivatives, and securitized debt.

The transcript also emphasizes that derivatives are not just tools for hedge funds. Airlines can hedge fuel-price risk by buying options tied to oil prices, and large companies and governments use options to manage specific exposures. Yet the same leverage and interconnectedness can amplify stress. During normal times, derivatives can add liquidity and stability; in abnormal times, many positions move together—often downward—creating conditions for sharper market dislocations.

Finally, the narrative returns to the “casino” theme: once pricing formulas are widely known, beating markets requires new pattern-finding. Jim Simons built Renaissance Technologies and the Medallion Investment Fund using machine learning and massive datasets, producing extraordinary returns for decades. The transcript closes by arguing that physicists and mathematicians didn’t just make money—they provided the models that define risk, price derivatives, and influence market structure. If all patterns were ever fully discovered, those patterns could be arbitraged away, leaving a truly efficient market where price changes are indistinguishable from randomness.

Cornell Notes

Options pricing became a trillion-dollar engine once finance learned to treat stock movements as probabilistic processes rather than guesswork. Louis Bachelier modeled stock prices as a random walk and used probability to compute a fair option price by equalizing expected returns for buyers and sellers. Ed Thorpe’s dynamic hedging idea—rebalancing a stock position as an option’s delta changes—showed how risk could be offset through trading. Fischer Black, Myron Scholes, and Robert Merton then produced the famous Black-Scholes-Merton framework, adding drift and using stochastic calculus to yield an explicit formula that made options pricing usable at scale. The result was explosive growth in derivatives markets and new ways to hedge risks, though leverage can also worsen crashes during stress.

Why did Louis Bachelier’s random-walk approach become central to option pricing?

How do call and put options limit downside while creating leverage?

What is dynamic hedging, and why does it matter for risk?

What changed when Black, Scholes, and Merton replaced Bachelier’s simpler model?

Why can derivatives stabilize markets in normal times but worsen crashes in stress?

How did Jim Simons’ approach relate to the “efficient market” debate?

Review Questions

- How does the strike price determine whether a call option’s buyer exercises, and how does that shape the option’s payoff profile?

- What assumptions about stock-price behavior distinguish Bachelier’s model from the Black-Scholes-Merton framework?

- Explain how dynamic hedging uses delta and rebalancing to reduce risk for an option seller.

Key Points

- 1

Bachelier’s random-walk model turned option pricing into a probability problem by linking future stock distributions to expected payoffs relative to the strike price.

- 2

Options cap downside to the premium (if they expire out of the money) while offering leverage when the underlying moves far enough to exceed the strike.

- 3

Dynamic hedging reduces option risk by continuously adjusting a stock position based on delta as prices change.

- 4

Black-Scholes-Merton’s breakthrough was producing an explicit, computable pricing formula using drift plus stochastic calculus, enabling rapid adoption.

- 5

Derivatives can add liquidity and stability in normal markets, but they can amplify crashes when many positions move together during stress.

- 6

The transcript contrasts widespread pricing knowledge with the need for new pattern-finding to beat markets, highlighting Jim Simons’ data-driven approach at Renaissance Technologies.

- 7

The derivatives industry’s scale—hundreds of trillions globally—reflects how options multiply exposure to underlying assets into many tradable risk profiles.